Introduction

Malaysia has a high level of digital adoption that hasfacilitated strong growth in the use of financial technologies(fintech) such as digital payments. The Central Bank ofMalaysia (Bank Negara Malaysia, BNM) has instituted anInteroperable Credit Transfer Framework (ICTF) that fostersinnovation and the development of other fintech services,such as digital banks and cross-border digital payments.

With the intention of expanding Malaysia’s participation inglobal finance and digital trade, both public and privateentities in Malaysia are exploring international partnershipsfor cross-border digital payments. This could improveMalaysia’s economic growth and expand its role in the globaleconomy.

When considering global digital finance, there are at least four policy issues to take into account,namely digital financial inclusion, increasing risks of financial cybercrime, disruptive effects ofunregulated decentralised finance and cryptocurrency, and geopolitical considerations.

In a four-part series on Malaysia’s expanding fintech and digital payments space, I assess thegrowth and current state of Malaysia’s digital adoption and use of the internet for financialtransactions and consider opportunities and initiatives in fintech, particularly in terms of crossborder digital payments. This is a fast-moving and fast-growing sector rapidly introducinginnovations and new technologies to consumers.

This first article in the series presents an overview of Malaysia’s digital adoption and useof fintech, focusing on the growth in digital payments from 2011–2024.

The second article reviews the contribution of BNM’s ICTF and the introduction of digital banksto Malaysia’s financial services landscape

The third article explores the demand for and developments in cross-border digital paymentsbetween Malaysia and other countries.

The fourth article discusses policy considerations around the use of digital payments and fintechin a globalised society.

Overview of Malaysia’s digital adoption and use

Malaysia has long had high rates of internet penetration and digital adoption1. In 2023, 97.1%2 ofpopulated areas had access to 4G mobile broadband coverage and approximately 96.4%3 ofhouseholds used the internet.

Between 2019 and 2022, broadband usage increased, notably during the Covid-19 pandemicwhen social distancing and movement restrictions forced people to rely on digital tools for workand school4. The overwhelming majority of Malaysians access the internet using theirsmartphones5, making the country a mobile-first nation where mobile broadband penetrationand/or subscription rates are higher than fixed broadband rates.

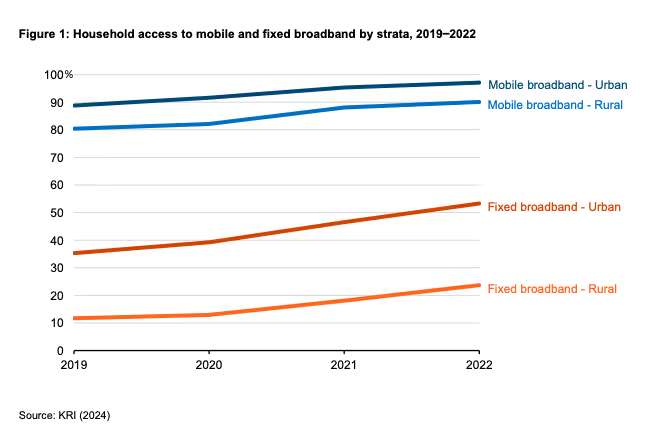

Figure 1 shows the share of households having access to mobile and fixed broadband from 2019to 2022. Mobile broadband use is clearly higher than fixed broadband use in both urban and ruralareas. The urban-rural gap for mobile broadband use is comparatively smaller than the urbanrural gap for fixed broadband use. Even though an urban-rural digital divide persists, mobilebroadband subscriptions for both groups have been consistently above 80% for the past fiveyears.

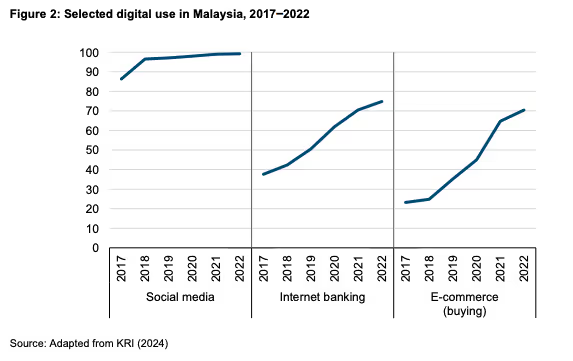

According to data from the Department of Statistics Malaysia (DOSM), the most common use ofthe internet among households is connecting and socialising with other people on social media.Figure 2 shows the rates of use for social media and two other popular uses of internet access,internet banking and online shopping, from 2017 to 2022. While social media use has been highfor a long time, reaching saturation well before the pandemic, the use of the internet for financialtransactions such as internet banking and online shopping experienced steady growth during thisperiod with room for further expansion

Growth of digital payments

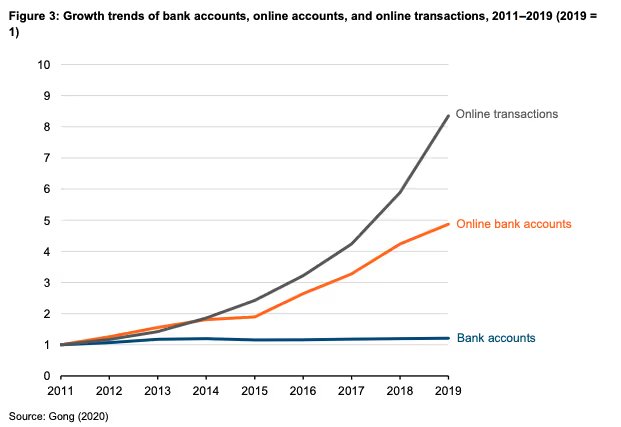

Data from BNM corroborate the DOSM data, showing that digital payment use has beenconsistently on the rise since well before 2019. Figure 3 shows the relative growth trends of bankaccounts, online bank accounts, and online transactions in the country from 2011 to 2019. Asmight be expected, the steep growth in the number of online transactions is accompanied by asteady increase in the number of online bank accounts while the number of bank accountsremains relatively constant.

The rise in online bank accounts suggests a growing appetite for digital payments and digitalfinancial services among the banked segment of the population. However, it is unclear if this canbe associated with increased financial inclusion. There is insufficient public data available toindicate whether the online transactions occur mostly across existing bank accounts or throughthe rise of other payment instruments, such as e-money via e-wallets (defined below).

Overview of retail payment systems in Malaysia

Note that BNM divides retail payments into three categories: payment systems, paymentinstruments, and payment channels6.

Payment systems comprise the shared infrastructure supporting financial transactions. Forexample, the Interbank GIRO (IBG) system supports funds transfers across its participatinginstitutions, while the Direct Debit payment system is an interbank collection service for repeatedpayments directly from a customer’s bank account to multiple banks with a single authorisation

Payment instruments comprise the tools used to conduct financial transactions, such as creditcards, debit cards and e-money.

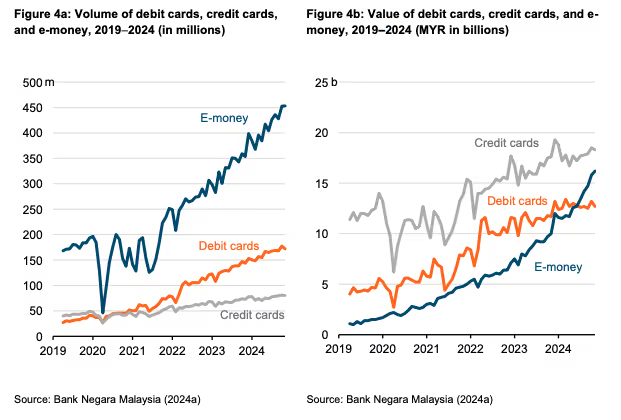

E-money is digital cash that has been pre-deposited, usually into an e-wallet or other digital app,by a user. This digital money can be used in place of physical cash to purchase goods and servicesand is deducted from the balance on the app, which is a form of network-based mobile payments.Digital money can also be linked with app-associated debit cards, blurring the lines between typesof payment instruments. Figures 4a and 4b show the trends in volume and value of transactionsvia debit cards, credit cards and e-money from 2019 to 2024.

The dip in volume in e-money transactions seen in Figure 4a is likely due to reductions in face-toface payments during movement restrictions caused by the pandemic, but growth quicklyrebounds. While volume of transactions for e-money grew more than both debit cards and creditcards, the total value of transactions for e-money has not yet caught up with that of credit cards.This suggests that people use e-money more for low-value payments and credit cards for highvalue payments.

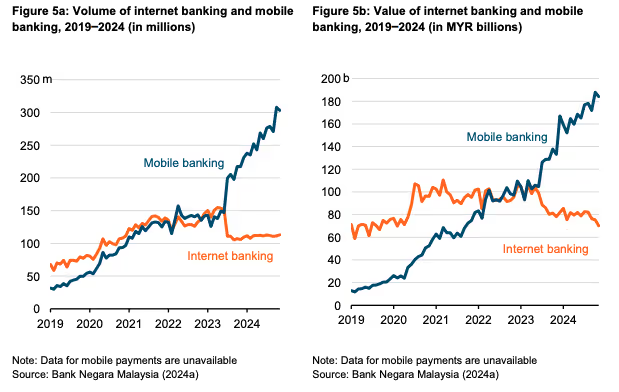

Payment channels are the means through which financial transactions are conducted, such asinternet banking, mobile banking and mobile payments. Internet banking is banking that isconducted using a computer with internet access, a web browser and a registered account forinternet banking services.

Mobile banking is similar to internet banking, but it is conducted using a mobile phone instead ofusing a web browser on a computer. Account registration for mobile banking is still a separatestep required by banks for security purposes.

Mobile payments are non-banking channels through which financial transactions are conductedusing a phone, typically using e-money as the payment instrument. However, data on the volumeand value of mobile payments are not available. Increasingly these distinctions are becomingmore blurred as payment systems become more interoperable, allowing different paymentinstruments to be used across different payment channels.

Figures 5a and 5b show the trends in volume and value of internet and mobile banking forindividuals from 2019 to 2024. As previously mentioned, Malaysia is largely a mobile-first nation,thus it is not surprising to see that mobile banking growth has been much greater than internetbanking growth and that internet banking has plateaued both in volume and value over the last two years

Conclusion

High levels of digital adoption in Malaysia have enabled the digitalisation of the financiallandscape, creating opportunities for economic growth, financial inclusion and transactionalefficiency. In particular, mobile digital payments, have gained currency (pun intended) in recentyears.

As more individuals and businesses adopt digital financial tools, the risk of cyber threats andfinancial fraud increases, potentially undermining public trust in digital financial systems.Balancing opportunities for growth with these risks is crucial to ensure that the digital financialecosystem is inclusive, secure and sustainable.

Thus, it is essential that stakeholders, including government, financial institutions, andtelecommunications providers, uphold robust regulatory frameworks, expand digital andfinancial literacy programs and strengthen cybersecurity safeguards. In this way, Malaysia canmaximize the benefits of digital adoption while mitigating associated risks.